First, the electrolytic copper market

This week, the Shanghai copper futures rose and fell, and the weekly high on Tuesday and Thursday, the copper price fell back to the previous increase on Wednesday, and the spot copper continued to rise 250 yuan this week. The spot copper fluctuated between 52000-53000 every week. The specific data are as follows: :

A new round of copper mine strikes in the foreign copper market will begin again. Union leaders said Chile's Codelco's Salvador copper miners began strikes in the early hours of Thursday, which accounted for 4% of Codelco's production. The world's largest copper mine, the Chilean Escondia copper miners, voted on the division of labor before September 6. If the vote is not passed, a second strike will be held. In addition, the salary negotiations of the Indonesian Copper Mines, the world's second largest copper mine, Freeport's McMullen Copper and Gold Company, have also reached a stalemate, not to rule out the mine production disruption or even the risk of unrest. If the strike is actually fulfilled, it is expected to stimulate the current weak copper price, or cause a temporary rebound in copper prices.

Second, the recycled copper market

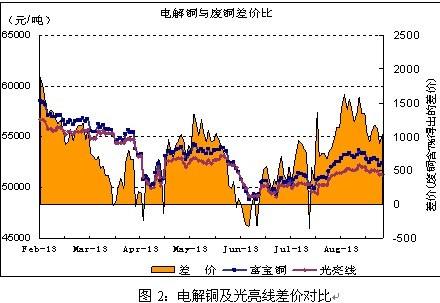

1, electrolytic copper and bright lines

This week, the price of scrap copper fluctuated within a narrow range, and the focus continued to move down. The market turnover remained deserted. Foshan's bright line averaged 48,170 this week, which was more obvious than last week's decline. The decline was less than 1%, and the shock was not sharp. From the figure, it can be clearly seen that the price of scrap copper has entered the adjustment area, and there is still a downward pressure on the short-term technical side. The refined price difference is gradually falling, indicating that the price of scrap copper has been bearish in the near term.

In the spot market of scrap copper, this week's scrap copper prices showed signs of resistance, so the price difference of refined scraps gradually narrowed. Since August, merchants and manufacturers have been more active in transactions, and the current supply on the market appears to be relatively tight. Since most merchants are still optimistic about the market outlook, the asking price is still firm, and the transaction is light this week. We recommend that businesses wait for the price of copper to stabilize and choose the right goods.

2, cable companies order to heat up

According to the tracking and investigation of cable enterprises in Shandong this week, the data shows that the average operating rate of 35 large and medium-sized enterprises is 66.42%. The annual production capacity of 6 large-scale enterprises is over 10,000 tons, with an average annual production capacity of 25,000 tons. The annual production capacity of 16 medium-sized enterprises is between 1000-10000 tons, with an average annual production capacity of 3,13.75 tons. There are 13 small-scale enterprises with an annual production capacity of 1,000 tons. Below, the average annual production capacity is as low as 410.3 tons.

Operating rate: In August (66.42%), the average operating rate in July was 62.33%, an increase of 4.09 points. Large and medium-sized enterprises have shown signs of recovery. The merchants reflected that there were three reasons for this: firstly, the price of copper at the beginning of the month drove some transactions in the market; secondly, although the high temperature troubles in the past few days prevented the construction site from starting or even stopping work, the cooling at the end of the month and the rise in copper prices boosted the operating rate gradually; Finally, due to the end of the so-called off-season, many companies have accelerated production waiting for "Golden September and Silver 10" to release more orders.

Third, the downstream market analysis

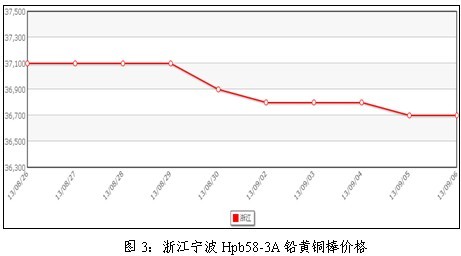

This week, Zhejiang Jinlong Hpb58-3 brass rod ex-factory price has once again moved down, mainly due to the increase in Syrian concerns this week, causing copper price shocks to fall, from the high near 7300 to the current 7100 US dollars, businesses frequently cut the price. The current price of brass rods is stable at 36,700 yuan / ton, and it is expected that there will be little room for further reduction next week.

At present, the summer is gradually turning cold, while the cable enterprise orders are entering the "warming" period. According to Fubao's survey data, in North China, where the start-up is relatively low, the operating rate in August increased by about 4% from the previous month, and the large cable factory started to return to 80%. The orders for SMEs also improved slightly. The rebound in copper prices and the retreat of high temperatures were all better than the start of the business. As a result, orders for major cable processing enterprises in China rose steadily in August, and some enterprises resumed to the level of construction in April and May. In the second half of the year, with the acceleration of infrastructure construction, cable usage will further increase, but it will not solve the problem of overcapacity in the cable industry. The copper price trend is still weak, and the country is accelerating the elimination of backward production capacity. Will gradually withdraw from the market.

Fourth, futures market analysis and forecast

This week, the price of copper fell back, and the center of gravity shifted slightly, in line with expectations. From the trend point of view, copper price was supported by the 40-day moving average, and the trend of the correction slowed down, as shown in the following figure:

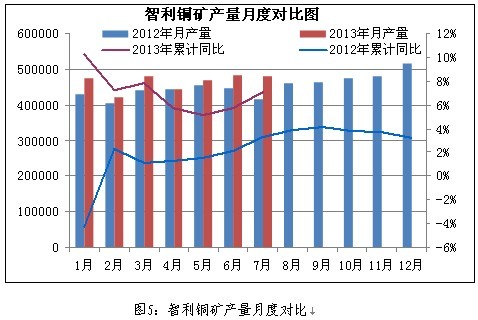

According to the report of the Chilean National Copper Council, Chile's copper output in January-July 2013 totaled 3.25 million tons, up 7% year-on-year, the largest increase since 2004. The monthly copper output was 480,440 tons, up 16% year-on-year. In terms of the mining area, the output of the Escondida mining area increased the most, with 100,000 tons; followed by the Collahuasi mining area, which increased production by 34,000 tons; the third was the increase of 28,000 tons of the Anglo American South Mine; the Esperanza mining area increased by 24,000 tons; the Candelaria Mine was 19,000 tons. The Los Pelambres mining area is 7,000 tons; the Chilean National Copper Company (Codelco) has an increase of 4,000 tons.

Excluding the factors affecting the relative low base of the previous year, Chile's new mine output increased significantly in 2013, and the grade of the old mines increased (sustainability is not high). The statistics of Chile's copper production in the previous July are as follows:

Although the copper price has been boosted by the recent favorable economic data, it has risen steadily; but due to the impact of supply and demand, the upward trend is expected to be relatively limited, and the rebound market must not be reversed. In the short-term, we will maintain the judgment of the technical shock of price fluctuations. It is expected that the weekly copper support level is 7000-7100 US dollars and the pressure level is 7300 US dollars; compared with the Shanghai copper period, the operating range is 5.1-5.25 million; the spot copper is 5.15-5.28 million; 4.65-4.85 million.

We supply various Power Distribution System products, including Electrical Metal Junction Box, Plastic Electrical Junction Box, Plug Adaptor, Circuit Breaker, Electrical Distribution Board etc.

If you want to know more about the products in Power Distribution System, please click the product details to view parameters, models, pictures, prices and other information about Power Distribution System, Electrical Distribution System, Ac Distribution System,

Dc Distribution System.

Whatever you are a group or individual, we will do our best to provide you with accurate and comprehensive message about Power Distribution System products.

Power Distribution System ,Electrical Distribution System,Ac Distribution System,Dc Distribution System

NINGBO LONGFLIGHT INTELLIGENT TECHNOLOGY CO.,LTD , https://www.long-flight.com